SECURE 2.0 New Tax Benefits for Retirement Savers

The benefits of setting aside funds in tax-advantaged accounts just got even better. The long-awaited SECURE 2.0 Act, enacted at the end of 2022, expands on the improvements made by the Setting Every Community Up for Retirement Enhancement Act of 2019 (the SECURE Act). Now you can save more and save longer for retirement, at a lower tax cost. Here are the highlights of the new law.

Saving more

Notably, the law contains provisions that enhance catch-up and matching contributions. Catch-up contributions are designed to help older retirement savers who didn’t set aside enough money earlier in their careers. For example, in 2023, you can contribute up to $22,500 to a 401(k) or similar employer-sponsored plan (up from $20,500 in 2022). Plus — if you’re 50 or older — you can make a catch-up contribution of up to $7,500 (up from $6,500 in 2022). For IRAs, the maximum contribution is $6,500 (up from $6,000 in 2022) plus a $1,000 catch-up contribution.

Under SECURE 2.0, starting next year, the catch-up amount for IRAs, which has stalled at $1,000 for many years, will be adjusted for inflation. In addition, starting in 2025, participants in 401(k) and similar plans who are 60 through 63 will be allowed to make catch-up contributions up to $10,000 (adjusted for inflation) or 150% of the regular catch-up amount, whichever is greater. Using the 2023 numbers for purposes of illustration, that would equate to a catch-up contribution of up to $11,250 ($7,500 x 150%).

Beware: Starting in 2024, catch-up contributions by highly compensated participants in employer plans will be required to make those contributions to a Roth account. In other words, these participants won’t be allowed to make catch-up contributions on a pre-tax basis. For purposes of this limitation, a highly compensated participant is one who earned more than an inflation-adjusted $145,000 from the plan sponsor in the previous year.

SECURE 2.0 also makes improvements to employer matching contributions. If permitted by the plan, employees may: 1) receive matching contributions in a Roth account, and 2) starting in 2024, treat certain student loan payments as contributions for matching purposes. This second provision allows employees to receive employer matches without having to decide between contributing to their retirement accounts and paying down student debt.

Saving longer

From a tax perspective, the longer you leave funds in an IRA or employer-sponsored retirement plan, the better. That’s because they continue to grow tax-deferred (or tax-free in the case of a Roth account), allowing your savings to multiply more quickly. Plus, for tax-deferred accounts, such as traditional IRAs or non-Roth employer plans, the longer you wait to withdraw the funds, the more likely you are to be in a lower tax bracket.

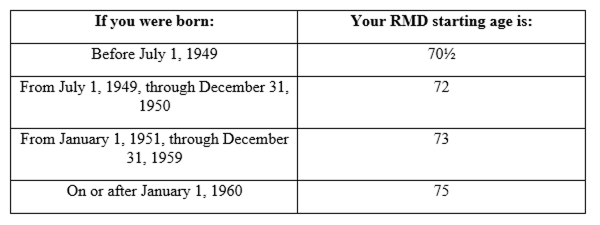

SECURE 2.0 allows you to save longer by increasing the age at which you must begin taking required minimum distributions (RMDs) from IRAs and employer-sponsored qualified retirement plan accounts. You may recall that the SECURE Act increased the RMD starting age from 70½ to 72, for taxpayers who turn 70½ after December 31, 2019. SECURE 2.0 raises the RMD starting age even further, first to 73 (for taxpayers who turn 72 after December 31, 2022) and later to 75 (for taxpayers who turn 73 after December 31, 2032). The following table shows the applicable RMD starting age according to your date of birth.

If your 72nd birthday is in 2023, you may have previously scheduled a distribution for this year based on prior law (which would have required an RMD by April 1, 2024). However, SECURE 2.0 gives you a one-year reprieve: Your first RMD won’t be due until April 1, 2025.

Other notable changes include:

- Reducing the penalty for a missed RMD from 50% to 25% of the amount that should have been withdrawn, and to 10% for taxpayers who correct the mistake on a timely basis, and

- Eliminating RMDs, beginning in 2024, for Roth accounts in employer-sponsored plans.

Saving for college

Section 529 college savings plans are a great tool. But if you don’t need all the funds for qualified educational expenses, withdrawals are subject to taxes and penalties.

SECURE 2.0 allows you to roll over unused 529 plan funds, tax- and penalty-free, into a Roth IRA for the same beneficiary. Rollovers are subject to annual limits on IRA contributions and a lifetime cap of $35,000 per beneficiary. In addition, the 529 plan must be at least 15 years old, and rollovers can’t be made from funds contributed within the previous five years (or earnings on those contributions).

Revisit your plan

These are just a few of the many tax benefits offered by SECURE 2.0. Your tax advisor can review your plan to ensure that you’re making the most of these benefits and maximizing your retirement savings.

Sidebar: Technical corrections required

It’s common for complex laws to contain mistakes, and SECURE 2.0 is no exception. As a result of apparent drafting errors in the law, there’s some ambiguity over when the starting age for required minimum distributions increases to 75. Although it seems clear that Congress intended it to apply to people who reach age 73 after December 31, 2032, the law says it applies to “an individual who attains age 74 after December 31, 2032.” Another apparent drafting error prohibits any catch-up contributions to employer-sponsored plans in 2024.

Congress is expected to make technical corrections to these provisions to ensure that the law works as intended. As of this writing, no corrections have been made. Contact your tax advisor for the latest developments.

This material is generic in nature. Before relying on the material in any important matter, users should note date of publication and carefully evaluate its accuracy, currency, completeness, and relevance for their purposes, and should obtain any appropriate professional advice relevant to their particular circumstances.

Share Post: